Unlocking India’s Carbon Credit Trading: A New Frontier for Renewable Energy Integration

“Carbon markets are no longer just climate instruments — they are becoming economic instruments.” That statement increasingly defines India’s evolving energy transition story. For decades, climate action was viewed as a cost to development. Today, it is rapidly transforming into a new marketplace where emissions themselves carry financial value. India’s emerging carbon credit trading ecosystem could become one of the most powerful drivers of renewable energy integration, industrial modernization, and green finance in the coming decade.

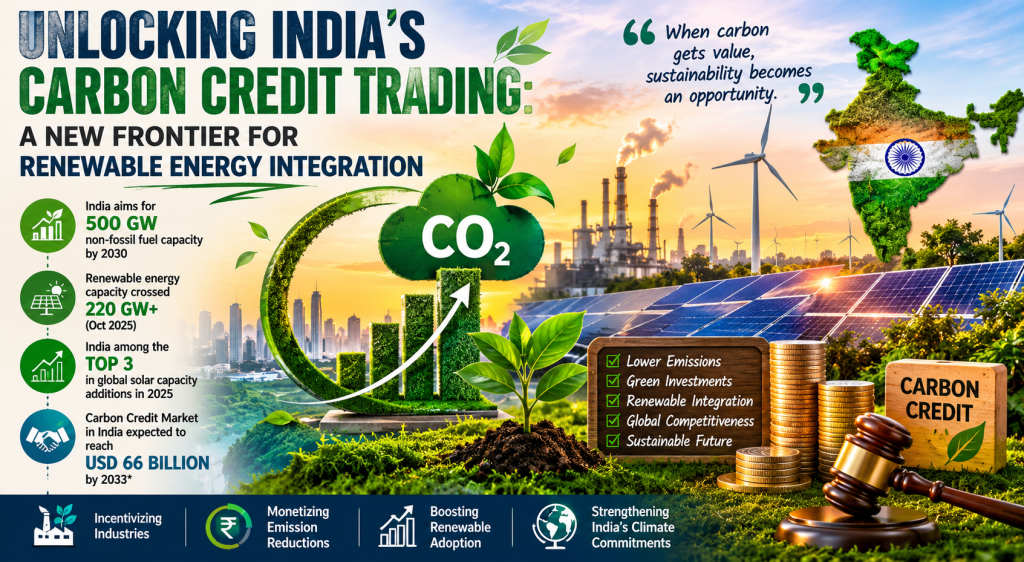

The timing could not be more critical. India is simultaneously the world’s fastest-growing major economy and one of the largest energy consumers. Electricity demand continues to surge as manufacturing expands, cities urbanize, and digital infrastructure scales. Yet India has also committed to ambitious climate goals, including a sharp reduction in emissions intensity and a massive increase in non-fossil fuel capacity. According to recent energy assessments, renewable energy generation in India rose nearly 20% in FY 2025–26, while coal generation growth slowed significantly.

At the center of this transition lies India’s Carbon Credit Trading Scheme (CCTS), introduced under the Energy Conservation (Amendment) Act, 2022. The framework marks India’s shift from purely regulatory climate governance toward a market-based emissions system. Under the scheme, industries that reduce emissions beyond prescribed limits can earn carbon credit certificates and trade them electronically through the Indian Carbon Market (ICM).

This may sound technical, but its implications are enormous. For the first time, Indian industries can potentially monetize decarbonization itself.

Imagine a textile unit in Surat replacing coal-fired boilers with biomass systems, or a dyeing cluster installing rooftop solar and wastewater heat recovery. Under a functioning carbon market, those emission reductions can translate into tradable financial assets. Suddenly, sustainability stops being merely a compliance exercise and starts becoming a revenue opportunity.

India’s renewable energy momentum is already accelerating at historic speed. The country recently overtook the United States to become the world’s second-largest market for annual solar capacity additions. Solar installed capacity crossed 132 GW in late 2025, while wind capacity surpassed 53 GW. According to the Ministry of New and Renewable Energy, India is targeting 500 GW of non-fossil fuel capacity by 2030 — one of the largest clean energy expansion programs globally.

But expanding renewable generation alone is not enough. The bigger challenge lies in integrating clean energy into industrial systems that still depend heavily on coal, furnace oil, and diesel. This is where carbon trading becomes transformational. By assigning economic value to emissions reduction, the market creates incentives for industries to adopt solar thermal systems, biomass fuels, energy-efficient motors, waste heat recovery, and electrified industrial processes.

The impact could be especially significant for India’s MSMEs. Small and medium enterprises contribute nearly 30% of India’s GDP and account for a major share of industrial energy consumption. Yet many MSMEs operate with outdated technologies and limited access to green finance. Carbon credits may provide an additional income stream capable of improving project viability for renewable energy adoption.

The stakes are becoming even higher because climate policy is now directly tied to international trade. The European Union’s Carbon Border Adjustment Mechanism (CBAM) is expected to impose carbon-linked costs on imports from carbon-intensive economies. Export-oriented Indian sectors such as textiles, chemicals, steel, and manufacturing are already facing mounting pressure to disclose and reduce emissions across supply chains.

“Green competitiveness will define future trade competitiveness,” many energy economists now argue — and India’s exporters are beginning to realize this rapidly.

The shift is already visible. Global buyers increasingly demand ESG disclosures, renewable energy sourcing, and Scope 3 emissions reporting from suppliers. What was once a voluntary sustainability discussion is now becoming a commercial requirement. Industries unable to measure emissions may soon struggle to access global markets.

India’s carbon market therefore serves a larger strategic purpose beyond climate mitigation. It is also about protecting industrial competitiveness in a decarbonizing global economy.

However, building a successful carbon market is far more complex than launching a policy notification. Carbon trading depends on robust monitoring, reporting, and verification systems. Industries must accurately measure emissions, verification agencies must validate reductions, and digital registries must ensure transparency and prevent double counting. The Bureau of Energy Efficiency has already outlined frameworks for Accredited Carbon Verification Agencies and electronic carbon credit registries, but institutional capacity remains a major challenge.

There is also the issue of awareness. Large corporations are gradually preparing for carbon disclosure and ESG compliance, but many MSMEs still lack basic understanding of carbon accounting. In industrial clusters across Gujarat, Maharashtra, and Tamil Nadu, smaller firms often see sustainability as an expensive obligation rather than a strategic investment opportunity.

Yet the economics may change quickly. Market projections suggest India’s carbon credit market could grow from nearly USD 6 billion in 2026 to over USD 66 billion by 2033. If even a fraction of this growth materializes, carbon finance could reshape investment decisions across manufacturing, infrastructure, and renewable energy deployment.

The broader macroeconomic context also favors this transition. India’s GDP growth remains among the highest globally, electricity demand continues to rise, and renewable technologies are becoming cheaper every year. Meanwhile, India’s emissions growth slowed sharply in 2025, marking the slowest increase in more than two decades outside the pandemic period. This signals that cleaner growth pathways are gradually becoming possible even within a rapidly industrializing economy.

Still, the road ahead is not guaranteed. Carbon prices must remain meaningful enough to influence industrial behavior. Renewable energy access must expand beyond large corporations into MSME clusters. Financing mechanisms must support smaller industries that cannot independently absorb green transition costs. Most importantly, policy stability will determine whether industries view carbon markets as long-term investment signals or temporary regulatory experiments.

India’s energy transition has often been described as a balancing act between development and decarbonization. Carbon trading may finally offer a bridge between the two. If implemented effectively, the Indian Carbon Market could become far more than a climate compliance mechanism. It could emerge as a financial engine that accelerates renewable energy integration, strengthens industrial competitiveness, and positions India as a leader in the next generation of green economic growth.

The real question is no longer whether India can afford to price carbon. Increasingly, it is whether India can afford not to.